Last year, chancellor Rishi Sunak announced that he would freeze Income Tax thresholds until 2026, and it means far more people will be paying the higher- or additional-rate tax in the future.

Coupled with the freeze, it’s anticipated that wages will rise at a faster pace than expected thanks to high levels of inflation and low levels of unemployment.

These factors could mean that you pay a higher rate of Income Tax than you expect.

According to an FTAdviser report, 1 in 10 taxpayers paid the higher rate of Income Tax in 2010/11. It’s estimated that by 2024/25, this will rise to 1 in 5.

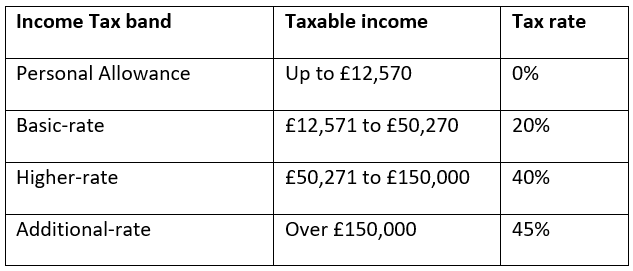

You pay Income Tax on all your income that is above the Personal Allowance, which is £12,570 for the 2022/23 tax year. It covers most types of income you may receive, including a salary and pension. So, even if you’re no longer working, you still need to consider how much Income Tax you will be liable for and the effect your decisions will have.

The below table shows the Income Tax thresholds and rates for 2022/23, which are expected to remain the same until 2026.

The tax rates and thresholds are different in Scotland, but inflation could still mean you’re pushed into a higher tax bracket.

5 ways you could reduce how much Income Tax you pay

Making use of allowances and managing your income can help you reduce how much Income Tax you pay, and could keep you in a lower tax bracket. Here are five options that may be right for you.

1. Take advantage of salary sacrifice schemes

If your employer offers salary sacrifice schemes, they can help to reduce your Income Tax liability.

As an employee, you give up part of your salary in exchange for other benefits, such as higher pension contributions from your employer or employer-provided childcare. As your income will be lower, salary sacrifice schemes can be used to reduce how much tax you pay and ensure your income remains below certain thresholds.

If you’re considering salary sacrifice, you should weigh up how valuable the benefits you’d receive in return are. In some cases, they may not be right for you.

2. Benefit from the Marriage Allowance

If you’re married or in a civil partnership, you may be able to take advantage of the Marriage Allowance to reduce the amount of Income Tax you pay overall as a couple.

The Marriage Allowance lets one person transfer up to £1,260 of their Personal Allowance to their partner if they don’t use it. During a tax year, this can save you up to £252.

3. Increase your pension contributions

A pension offers you a tax-efficient way to save for your future.

Contributions you make to your pension will benefit from tax relief; this effectively means the money you’ve paid in tax is added to your retirement savings. As your pension is typically invested, the tax relief could grow further.

Tax relief is available at the highest rate of Income Tax you pay. If you’re a basic-rate taxpayer, it will usually be claimed automatically on your behalf. If you’re a higher- or additional-rate taxpayer, you will need to complete a self-assessment tax form to claim the full amount you’re entitled to.

Keep in mind that you cannot access your pension savings until you reach pension age, which is 55, rising to 57 in 2028.

4. Save in a tax-efficient way

Most people don’t pay tax on the interest they earn on savings.

The personal savings allowance (PSA) is the amount you can earn in interest without paying tax on it. How much the allowance is depends on what rate of Income Tax you pay:

- Basic-rate taxpayers: £1,000

- Higher-rate taxpayers: £500

- Additional-rate taxpayers: £0

It’s estimated that the PSA means 95% of people don’t pay tax on their savings. If you’re among the 5% that could be liable, moving your savings to a tax-efficient wrapper makes sense. Each year you can add up to £20,000 to an ISA. You do not pay Income or Capital Gains Tax on interest or returns from investments held in an ISA.

5. Use dividends to create an income

If you hold dividend-paying investments or are a business owner, you may be able to use dividends to boost your income without having to pay Income Tax.

The Dividend Allowance means you can receive up to £2,000 in dividends in the 2022/23 tax year before tax is due. If you exceed this threshold, you will be liable for Dividend Tax, and the rate may be lower than your Income Tax rate.

A bespoke financial plan can help you reduce tax liability

Depending on your circumstances, there may be other steps that you can take to reduce your tax liability. For example, if you’re self-employed, you may be able to deduct some expenses from your tax bill.

Please contact us to discuss your options and create a plan that will help you get the most out of your income and assets.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.